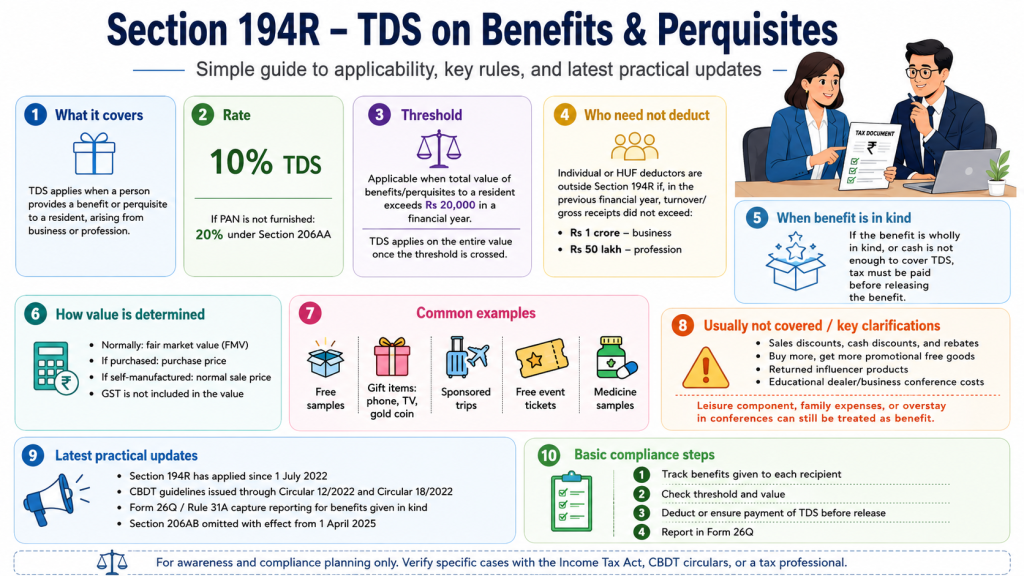

1. 📍 What is Section 194R?

Section 194R is a provision in the Income‑tax Act, 1961 that requires tax to be deducted at source (TDS) when a person provides any benefit or perquisite (in cash or kind) to a resident arising from a business or profession.

➡️ It applies regardless of whether the benefit is cash or non‑cash (for example gifts, free trips, gadgets, free samples, vouchers, etc.).

2. 📅 When Did It Become Effective?

- The section was introduced through the Finance Act, 2022.

- It came into force from 1st July 2022.

3. 🧾 Why Was Section 194R Introduced?

The main purpose is to prevent tax avoidance and broaden the tax base by capturing non‑monetary benefits that previously might not have been reported as income.

Before this, benefits like free products or perks were often claimed as business expenses and not separately taxed, leading to reporting gaps.

4. 📌 Who Must Deduct TDS Under Section 194R?

✅ Persons Required to Deduct TDS

Any person (including businesses, companies, individuals/professionals) who provides benefits/perquisites to a resident as part of business or profession must deduct TDS.

❗ Exceptions for Individuals & HUFs

Individuals or Hindu Undivided Families (HUFs) do not need to deduct TDS if:

- Their business turnover is below ₹1 crore, or

- Their professional gross receipts are below ₹50 lakh, in the previous year.

This exemption does not apply to companies, firms, and larger entities.

5. 📈 Applicability – When Does Section 194R Apply?

🔎 Conditions for Applicability

TDS under Section 194R applies if all of the following are true:

- A benefit or perquisite is provided by the payer.

- The benefit is provided to a resident person.

- The benefit arises in the course of business or profession.

- The total value of benefits to that person exceeds ₹20,000 in a financial year.

6. 💰 Threshold & Rate of TDS

- 🚫 Threshold: No TDS if total value ≤ ₹20,000 per person in a financial year.

- 📊 Rate: 10% TDS on the value of benefits exceeding ₹20,000.

- ⏱ When to Deduct: TDS must be deducted before providing the benefit or perquisite.

7. 📌 What Counts as a “Benefit or Perquisite”?

Examples include:

✔ Free gifts such as gadgets, appliances, gold coins

✔ Free or subsidised travel

✔ Sponsored business trips

✔ Vouchers or coupons

✔ Free samples provided to customers (e.g., medical samples to doctors)

✔ Club memberships or perks beyond ordinary deductions

❌ What Does Not Count

- Sales discounts, cash discounts, or rebates tied directly to purchase prices are not subject to 194R.

- “Buy one get one free” type discounts generally don’t trigger TDS.

- Ordinary employee benefits are not under Section 194R — they’re handled under Section 192.

8. 📊 How to Compute the Taxable Value

- Use the fair market value (FMV) of the benefit/perquisite.

- If the giver purchased the item, the actual purchase price may be used.

- If the giver manufactures the benefit (e.g., own product), then the standard selling price may be used.

Example:

Company gives a free laptop worth ₹25,000 to a business partner:

- Threshold: ₹20,000

- TDS taxable portion: ₹25,000 – ₹20,000 = ₹5,000

- TDS @10% = ₹500 to be deducted before giving the laptop.

9. 🧾 Filing & Compliance

📌 TDS Return

- File quarterly TDS returns using Form 26Q.

📌 TDS Certificate

- Issue Form 16A to the recipient for TDS deducted.

10. 📌 What Happens If You Don’t Deduct TDS?

Penalties for non‑deduction or delayed deposit may include:

✔ Interest on late TDS deposit

✔ Fines or penalties for non‑compliance

✔ Difficulty for the recipient in claiming TDS credit

The Income Tax Department may issue notices if compliance isn’t done properly.

11. 📌 Practical Compliance Tips

✔ Maintain records of all perks and benefits given.

✔ Calculate value and TDS before releasing benefit.

✔ Collect recipient PAN details to avoid higher TDS (20%).

✔ Classify each benefit as business‑related (eligible) or non‑business (not eligible).

12. 📌 Recent Updates or Reclassification (Important)

Note: Some compliance systems and tax filing challans have been updated in recent tax rules. For example:

- New TDS Payment Codes (like 1033/1034) may replace older references to Section 194R.

- New forms like Form 131 may be used for certificates instead of Form 16A (but the rate, threshold & core requirement remain the same).

These updates are more about filing formats and do not change the underlying tax deduction requirement.

✅ In short:

Section 194R makes it mandatory to deduct 10% TDS on any non‑monetary or monetary perks/benefits given during business or profession when the annual total per person exceeds ₹20,000.

It’s about transparent reporting and preventing tax avoidance on benefits that would otherwise escape taxation.

This guide explains Section 194R clearly and helps readers understand TDS applicability on benefits and business perquisites easily.