Introduction

Investing in the stock market can often feel like navigating a complex maze, especially for beginners. The constant ups and downs of stock prices, combined with an overwhelming amount of financial jargon, frequently cause new investors to hesitate or avoid taking action altogether. However, building long-term wealth does not require you to time the market perfectly or possess a massive amount of starting capital. There is a practical, structured, and highly accessible pathway that simplifies this entire journey for everyday individuals: the Systematic Investment Plan.

A Systematic Investment Plan, universally known as a SIP, has fundamentally transformed the way modern retail investors approach equity markets. Instead of waiting to accumulate a large lump sum of money or trying to guess when stock prices will hit their lowest point, a SIP allows you to invest fixed amounts of money at regular intervals. This straightforward mechanism takes the guesswork out of investing, turning wealth creation into an automated, stress-free habit. It is precisely why millions of salaried professionals, students, and first-time investors across India choose this method to secure their financial futures.

Understanding the underlying mechanics of how a SIP operates within the broader stock market ecosystem is critical before you commit your hard-earned money. By learning how your regular monthly contributions translate into shares or mutual fund units, you gain the confidence needed to stay invested during volatile market phases. In this comprehensive master guide, we will break down the foundational concepts, explore the mathematical power of compounding, weigh the distinct advantages alongside the inherent risks, and provide you with a practical roadmap to launch your own successful investment journey.

What Is SIP (Systematic Investment Plan)?

At its core, a Systematic Investment Plan is not an investment asset class in itself, but rather a smart, disciplined methodology of investing money. Many beginners mistakenly confuse a SIP with a standalone financial product, often asking whether they should buy a mutual fund or a SIP. To clear up this common misconception, think of a mutual fund as a destination—a basket of diversified stocks—and a SIP as the reliable vehicle that takes you there step-by-step.

When you opt for a SIP investment explained in its simplest terms, you commit to investing a specific, predetermined amount of money into a chosen financial instrument on a fixed schedule. This frequency is most commonly monthly, though it can also be weekly or quarterly, depending entirely on your cash flow and personal preference. The beauty of this framework lies in its sheer accessibility. In India, you can initiate a monthly SIP investment with amounts as low as ₹500, making it an incredibly democratic tool that fits comfortably into any household budget.

By choosing a SIP for beginners, you transition away from the high-stress world of active stock trading and enter the realm of automated asset accumulation. Your contributions are automatically channeled into equity mutual funds or exchange-traded funds (ETFs) which hold shares of various companies. Consequently, you do not need to spend hours analyzing balance sheets or monitoring live price charts. Professional fund managers handle the stock selection on your behalf, while your SIP ensures that you consistently buy into the market through all its natural economic cycles.

How SIP Works in Stock Market Investing

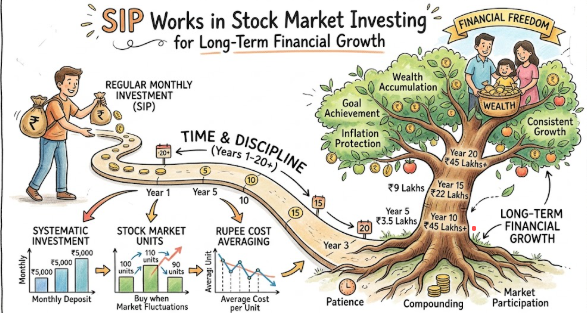

To truly appreciate the elegance of a systematic investment plan in stocks, you must understand how your money interacts with fluctuating market values. Every single time your scheduled SIP installment is processed, your money purchases units of a specific mutual fund scheme. The cost of a single unit of a mutual fund is known as its Net Asset Value (NAV). The NAV changes every single business day based on the closing prices of the underlying stocks held within that fund’s portfolio.

Because market prices are always moving, a fixed monthly investment will naturally buy a varying number of fund units each month. This dynamic introduces the core operational pillar of a SIP, known as Rupee Cost Averaging. When the stock market goes through a correction or a bearish phase, stock prices drop, causing the fund’s NAV to fall. Because the NAV is lower, your fixed monthly allocation automatically purchases a higher number of units. Conversely, when the market experiences a bullish surge and prices soar, your fixed allocation buys fewer units because each unit costs more.

Over a long-term investment SIP horizon, this continuous alternating cycle works heavily in your favor. You naturally end up acquiring more units when prices are cheap and fewer units when prices are expensive. Over time, the average cost per unit of your entire investment portfolio tends to be significantly lower than the average market price during that same period. This eliminates the psychological pressure of trying to time the market perfectly, ensuring that short-term volatility actually becomes an active tool for lowering your overall acquisition cost.

Furthermore, this continuous acquisition feeds directly into stock market compounding SIP dynamics. As you accumulate more units month after month, the fund houses pass along any underlying corporate dividends or capital gains by reinvesting them directly back into the fund, which increases your overall asset base. Compounding occurs when the returns generated by your investments begin earning returns of their own. Over a prolonged timeline, this compounding loop snowballs, transforming modest, routine monthly allocations into substantial financial portfolios.

Benefits vs Risks of SIP

| Aspect | Benefits | Risks |

| Rupee Cost Averaging | Reduces impact of market volatility | Returns fluctuate with market |

| Disciplined Investing | Encourages regular investing | Commitment required every month |

| Compounding Effect | Wealth grows over time | Long-term commitment needed |

| Flexibility | Can start/stop as needed | Early withdrawal may reduce gains |

| Affordability | Invest small amounts | Inflation can affect real returns |

| Diversification | Spread across stocks/funds | Fund selection risk |

Step-by-Step SIP Process

Setting up a Systematic Investment Plan is remarkably straightforward, thanks to modern digital banking and investment infrastructure. Here is the sequential process you need to follow to move from a beginner to an active investor:

- Assess Your Goals and Risk Profile: Before looking at any fund charts, clearly define why you are investing and how much volatility you can comfortably handle. Are you investing for a down payment on a house in five years, or are you building a retirement fund for twenty years down the line? Your timeline directly dictates the level of risk you should take.

- Choose the Right Mutual Fund or ETF: Based on your risk assessment, select an appropriate equity mutual fund scheme. Beginners often start with large-cap index funds, which invest in India’s top 50 or 100 largest companies, offering relatively stable growth compared to mid-cap or small-cap funds.

- Decide the Monthly Investment Amount: Analyze your monthly income and expenditures to determine a comfortable, sustainable investment amount. Remember, consistency is vastly more important than the size of the initial amount; it is better to sustain a smaller SIP for years than a large one for only a few months.

- Select Your Frequency and Investment Date: Pick a specific date for your monthly allocation to execute. It is a highly effective strategy to schedule this date a few days after your regular monthly salary or primary income hits your bank account, ensuring the funds are readily available before you spend them elsewhere.

- Set Up an Auto-Debit (Bank Mandate): Authenticate a recurring e-mandate or auto-debit facility through your net banking or UPI platform via your chosen investment app. This step automates the entire process, allowing the bank to seamlessly transfer your chosen amount directly to the fund house every month without requiring manual intervention.

- Track and Review Periodically: Once your auto-debit is active, your primary job is to let the system run smoothly. Monitor the account periodically—ideally once or twice a year—to ensure the transactions are processing correctly and the fund continues to align well with your broader financial objectives.

How SIP Helps Beginner Investors

For individuals who are entirely new to the financial markets, a SIP acts as an excellent educational bridge and protective shield. The stock market can be intensely emotional; seeing asset prices fluctuate daily frequently prompts beginners to make hasty decisions, such as selling out of fear during a temporary market dip or buying at record highs due to media hype.

A SIP introduces a structured environment that effectively mitigates these pitfalls through several key mechanisms:

- Low Capital Requirement: It shatters the myth that you need large sums of money to participate in corporate India’s growth, allowing you to learn the ropes of investing using minor chunks of discretionary income.

- Cultivates Financial Discipline: By treating your investment as a non-negotiable monthly expense that leaves your account right after payday, it naturally builds a powerful habit of saving first and spending what remains.

- Provides Measured Market Exposure: Instead of risking a large amount of capital all at once in an unfamiliar environment, you slowly dip your toes into the equity markets, getting accustomed to volatility over time.

- Removes Emotional Decision-Making: Because the entire process is automated, you eliminate the daily internal debate over whether today is a “good day” or a “bad day” to buy stocks, keeping your long-term plan perfectly on track.

Common Mistakes to Avoid in SIP

Even with the inherent simplicity of a Systematic Investment Plan, many well-intentioned investors fail to achieve their desired financial outcomes because they fall into predictable behavioral traps. Being aware of these missteps in advance is the best way to safeguard your financial future.

- Stopping the SIP During Market Downturns: This is the absolute most common mistake made by beginners. When the stock market crashes, panic sets in, and many investors pause their allocations to “prevent further losses.” By doing this, you completely miss out on the primary mechanism of Rupee Cost Averaging, failing to buy units when they are at their cheapest.

- Expecting Quick, Guaranteed Returns: A SIP in equity mutual funds is fundamentally designed for long-term horizons. Expecting massive profits within a year or two often leads to deep disappointment, as equity markets require time to smooth out short-term fluctuations and unlock compounding benefits.

- Choosing Funds Based Solely on Past Returns: Many beginners simply look at a list of funds, sort by the highest return over the previous 12 months, and invest immediately. However, the top-performing fund last year often operates in a highly cyclical sector that might underperform over the next three years.

- Failing to Step Up Investments Over Time: As your career progresses and your salary naturally increases, keeping your SIP amount completely stagnant limits your ultimate wealth potential. It is highly beneficial to utilize a ‘Step-Up SIP’, increasing your monthly contribution by a small percentage annually to keep pace with your rising income and combat inflation.

- Ignoring the Inherent Fund Risk Profile: Investing heavily in high-risk sectors or small-cap funds when you have a very short investment timeline or a conservative risk tolerance can lead to severe stress and unexpected capital erosion when market cycles turn.

SIP Beginner Checklist

| Checklist Point | Status |

| Fund selected based on goals | Yes/No |

| Monthly investment amount decided | Yes/No |

| Auto-debit or recurring setup | Yes/No |

| Investment frequency fixed | Yes/No |

| Risk profile considered | Yes/No |

| Review period planned | Yes/No |

| Performance tracking | Yes/No |

| Portfolio diversification checked | Yes/No |

| Emergency fund in place | Yes/No |

| Long-term commitment understood | Yes/No |

Real-Life Example: The Journey of a Salaried Professional

To visualize exactly how these abstract concepts manifest over a realistic timeframe, let us look at the practical case of a salaried professional named Rahul. At 25 years old, Rahul secured his first steady job in Bengaluru. After covering his rent, utilities, and lifestyle expenses, he realized he could comfortably set aside ₹5,000 every single month. Instead of leaving this money idle in a standard savings account, he decided to launch a monthly SIP investment into a diversified equity mutual fund.

During the first year of Rahul’s investment journey, the stock market entered a prolonged bearish phase due to global economic headwinds. Rahul watched the total current value of his portfolio drop below the actual amount of cash he had contributed. While a friend of his panicked and shut down his own accounts, Rahul recalled the mechanics of Rupee Cost Averaging. He maintained his composure and allowed his monthly auto-debit to continue uninterrupted, quietly accumulating a high volume of fund units at a heavily discounted NAV.

By the third and fourth years, the economic cycle turned around completely. The stock market staged a powerful recovery, and the NAV of Rahul’s chosen mutual fund rose substantially. Because he had aggressively accumulated a vast number of units when prices were low, the overall value of his holdings surged dramatically. The compounding effect began to display its strength, as the returns generated in the earlier years were now actively generating gains of their own on top of his ongoing monthly contributions.

By the time Rahul reached his 30th birthday, completing exactly 5 years of disciplined investing, he had contributed a total principal amount of ₹3,00,000. Because he remained absolutely consistent through both the market corrections and the market surges, his portfolio value had grown substantially, outperforming traditional fixed deposits by a wide margin. This accumulation provided him with a robust financial cushion and, more importantly, gave him firsthand proof of how discipline and patience form the true cornerstone of equity wealth creation.

Practical Tips for SIP Investors

Achieving long-term financial success via a Systematic Investment Plan requires a blend of the right strategies and the right mindset. Here are several actionable, high-impact tips to help you maximize your wealth-creation journey:

- Prioritize an Early Start: The sooner you begin your SIP, the more time your money has to benefit from compounding. Starting with a smaller amount in your early twenties can frequently yield a significantly larger final corpus than starting with a much larger amount in your mid-thirties.

- Automate to Eliminate Discipline Friction: Do not rely on manual monthly transfers, which require you to actively make a decision every month. Use the auto-debit feature so your investment becomes a permanent, seamless background process that happens automatically.

- Maintain True Diversification: Avoid allocating all your SIP money into a single fund or a single specific sector. Instead, spread your capital across complementary styles, such as pairing a stable large-cap index fund with a well-managed flexi-cap fund.

- Tune Out Daily Financial Media Noise: Sensationalist news headlines predicting immediate market crashes or overnight booms are designed to capture short-term attention. As a long-term SIP investor, these daily fluctuations are merely noise that you can safely ignore.

- Keep an Emergency Fund Separated: Always ensure you have three to six months’ worth of essential living expenses parked securely in a liquid savings account or liquid fund before starting your SIP. This ensures that if you face an unexpected medical cost or job transition, you will never be forced to break your long-term SIP prematurely to cover immediate bills.

When Should You Avoid SIPs?

While a Systematic Investment Plan is an incredibly versatile and powerful tool for the vast majority of retail investors, it is not an absolute silver bullet for every single financial scenario. There are specific circumstances where committing your money to a long-term equity SIP can actually be counterproductive or introduce unnecessary financial strain.

First and foremost, you should avoid equity SIPs if you have a very short-term need for that specific cash. If you are saving up for a wedding, a down payment on a car, or a university tuition fee that needs to be paid within the next twelve to twenty-four months, the stock market is simply too unpredictable. A sudden market correction right before your payment deadline could erase a chunk of your capital, leaving you short of your goal. For short horizons, capital preservation should take priority over growth, making predictable instruments like fixed deposits or liquid debt funds a far safer choice.

Secondly, a SIP is highly dependent on a regular, predictable inflow of capital. If you are currently facing an emergency financial crisis, managing high-interest debt like credit card dues, or dealing with highly volatile, inconsistent income streams without a safety net, forcing a monthly investment commitment can jeopardize your short-term financial stability. It is always a wiser financial move to pay off expensive debt and secure your basic livelihood security before attempting to build a long-term investment portfolio.

Frequently Asked Questions (FAQ)

1. What exactly is a SIP and how does it differ from a mutual fund?

A SIP is a systematic method of investing, whereas a mutual fund is the actual investment product. A SIP allows you to buy into a mutual fund gradually over time rather than investing a large lump sum all at once.

2. Can I lose money in a Systematic Investment Plan?

Yes, because SIPs invest directly in stock market instruments, your portfolio value will fluctuate based on market performance. However, holding your investments over a long-term horizon significantly reduces the likelihood of experiencing a net loss.

3. What is the minimum amount required to start a monthly SIP investment in India?

Most mutual fund houses in India allow investors to start a monthly SIP with as little as ₹500. This low barrier to entry makes it easy for students and young professionals to build consistent investing habits early.

4. Can I pause or stop my SIP if I face a temporary cash crunch?

Yes, SIPs offer excellent operational flexibility. You can easily pause, modify, or completely stop your regular monthly contributions through your investment platform without facing penalties, and your existing accumulated units will remain safely invested.

5. How long should I hold a SIP to see the real benefits of compounding?

While you can invest for any duration, the true exponential benefits of compounding generally begin to show prominently after a period of 7 to 10 years, as the returns generated begin to dwarf your actual out-of-pocket principal contributions.

6. What happens if I miss a single scheduled SIP auto-debit date?

If your bank account lacks sufficient funds on the debit date, the mutual fund house will simply skip that month’s transaction without canceling your plan or charging a penalty. However, your commercial bank may levy a standard bounce charge for a failed auto-debit instruction.

7. Is a SIP eligible for any tax deductions under Indian income tax laws?

Yes, contributions made specifically into Equity Linked Savings Schemes (ELSS) mutual funds via a SIP are eligible for tax deductions under Section 80C of the Income Tax Act. Keep in mind that ELSS funds come with a mandatory three-year lock-in period.

8. Is it possible to change the monthly investment amount later on?

Yes, you can easily adjust your SIP amount. If your income increases, you can set up a new SIP or utilize a step-up feature; if you need to scale back your budget, you can cancel the current mandate and initiate a smaller monthly amount.

9. Which is better for a beginner: a lump sum investment or a SIP?

For the vast majority of beginners, a SIP is significantly better. It eliminates the high-stress requirement of trying to time the market perfectly, protects you from emotional decision-making, and allows you to build wealth smoothly using small portions of your regular income.

10. How can I monitor the performance of my active investments?

You can easily track your consolidated portfolio, average purchase costs, total units accumulated, and real-time absolute or annualized returns through your investment platform’s digital dashboard or by reviewing your monthly account statements.

Conclusion

Mastering how SIP works in stock market investing is one of the most impactful steps you can take toward achieving genuine financial independence. By shifting your focus away from the chaotic, unpredictable daily movements of individual stock prices and focusing instead on automated consistency, you unlock a stress-free framework for long-term growth. Through the reliable mechanisms of Rupee Cost Averaging and the compounding effect, modest monthly contributions can steadily transform into a substantial financial foundation over time.

The most critical factor in a successful investment journey is simply getting started. Waiting for the “perfect” market condition or a larger salary often leads to costly delays that diminish your ultimate wealth potential. By committing to start small, staying consistent through all market phases, and regularly reviewing your progress, you take full control of your financial trajectory.

I’ve seen that many investors don’t review fund performance periodically. Blindly continuing SIPs without checking fund quality can lead to suboptimal outcomes.